BLOG

Blog

In response to our “As the Affordable Housing Crisis Worsens, Innovative Property Managers Could be a Solution” post from April, our friends at Money.com reached out to share some of their research. As the rental market has picked up over the past few months, more questions regarding rental insurance was brought to the forefront. The Money.com team has recently updated and wished to share their research about renters insurance that includes insights on how it works, the best options in the market and what specific companies and plans offer. To read more about it, please click the following link: https://money.com/best-renters-insurance/?fbclid=IwAR2hu5SjgvY7w9fhL7C-yJBKZpBiRkJAQCiBWG5b5gww1O_uCulSdJHo51k

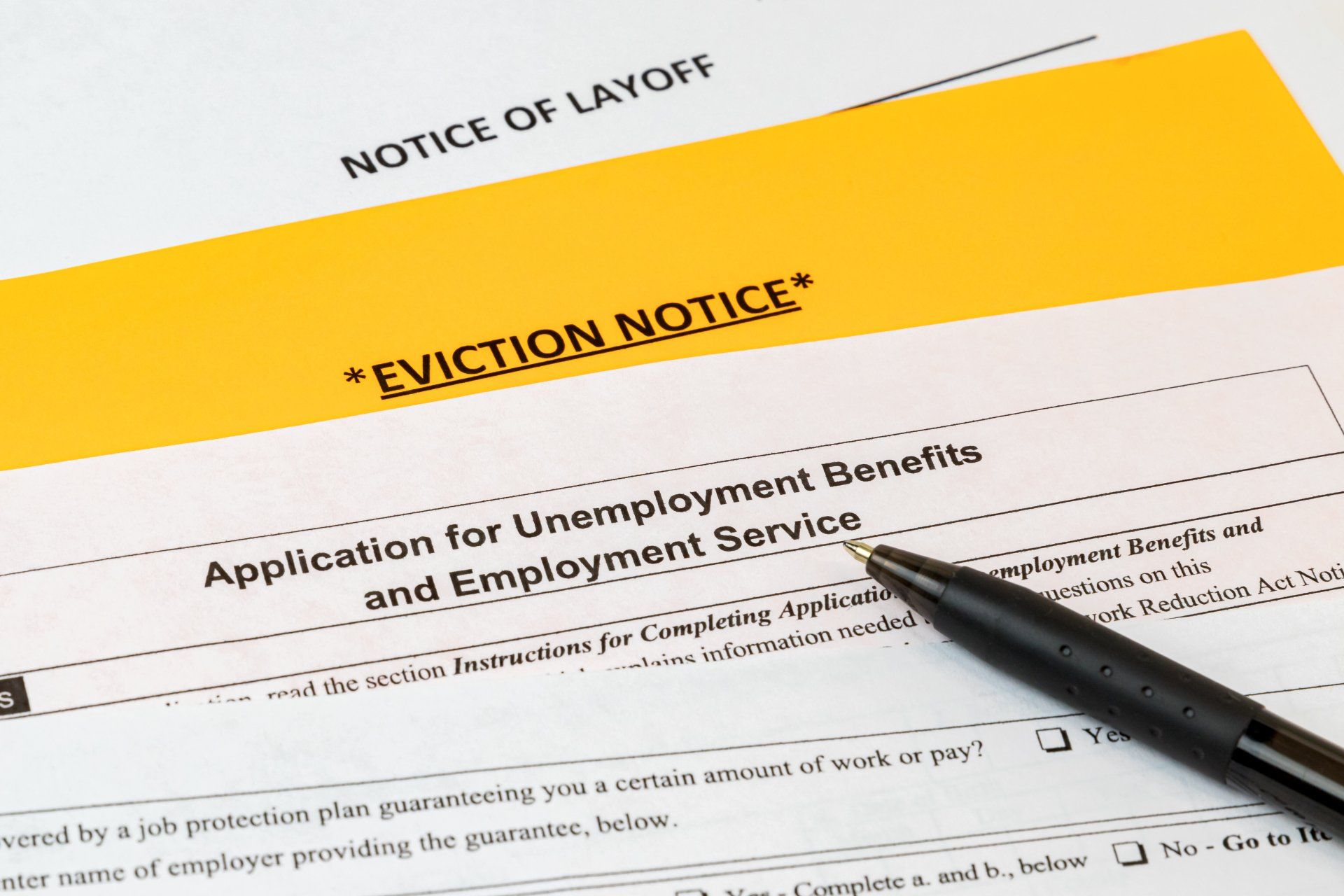

The Coronavirus Aid, Relief and Economic Security (CARES) Act passed in March of this year provided unemployed Americans $600 per week in addition to their state unemployment benefits. It is believed this assistance kept the U.S. rental market afloat. The Act also delivered legal protection for a host of renters and mortgage-holders with eviction moratoriums and mortgage relief. However, this assistance is due to run its course at the end of July. And with 45 million Americans filing jobless claims since March, there is a lot of worry of what comes next and how that will affect the U.S. rental market. Will more assistance come from the Federal Government? What’s the Federal Government’s next move is the big question. In May, the House of Representatives passed the latest coronavirus relief bill. This new bill called the Health and Economic Recovery Omnibus Emergency Solutions Act, or the "HEROES Act" is a $3 trillion stimulus package that exceeds the cost of the $2.2 trillion CARES Act. It is the largest stimulus bill in U.S. history. The Act offers a larger payment than the CARES Act as each member of a household would receive $1,200 - including children. The HEROES Act would be capped at $6,000 per household and the income thresholds would remain the same as the CARES Act. The new legislation, in its current form, would also provide $100 billion in rental assistance and a new 12-month eviction moratorium that also includes protections relative to forbearance. The legislation has not been picked up for vote in the Senate and there seems to be grumblings about the additional costs of the package. At the moment, the point of contention is the continuation of the federal unemployment benefit of $600 per week. It is reported that the Trump Administration and some Senate Republicans have voiced their disapproval of assistance going forward. The grievances have ranged anywhere from its effect on the U.S. Debt to creating disincentives for unemployed workers to go back to work. News outlets have reported that the Administration has mulled over the idea of creating a “cash bonus” program for those returning to work. What are the other options being proposed? We don’t know what parts, if any, of the Heroes Act would be passed in a Senate bill. But we can look at the latest proposed rental assistant bills introduced in the Senate. Ohio Democratic Senator Sherrod Brown announced May 4 on Twitter his “Emergency Rental Assistance and Rental Market Stabilization Act” which would direct $100 billion in emergency rental assistance to low-income renter households. The Act would give the Department of Housing and Urban Development (HUD) oversight over the distribution of funds. The funds would go directly to property owners or housing providers on behalf of renters. The next day Senator Jack Reed of Rhode Island introduced the $75 Billion Housing Assistance Fund to help protect renters, homeowners, and communities by preventing avoidable foreclosures, evictions, and utility shut offs. The Housing Assistance Fund would provide federal assistance to all state-level Housing Finance Agencies (HFAs) to help people remain in their homes as they try to get back to work. These funds could be put towards “mortgage payment and rental assistance; utility and internet payments; and other support to prevent eviction, mortgage delinquency, default, or foreclosure, or loss of utility services.” What to take from this? We should realize that one-time stimulus checks or bonuses will in no way be the lifeline to help unemployed Americans pay their rent for the foreseeable future. There has been hope for a quick recovery but recent coronavirus second-wave spikes in southern and southwestern states have shown that those forecasts may have been premature. There is a growing realization that the negative economic effects of this pandemic will be felt for a considerable amount of time.

Experts may not agree on how long the effects of the coronavirus may persist on our everyday lives. But one thing is for sure, the spread of COVID-19 and the social distancing practices now implemented will change the renting process for the foreseeable future. The way we shop for a home has been reconstructed overnight. The world has been put on hold and your ability to see the place you want to call home now comes with unforeseen obstacles. What processes, if any, have been put in place to allow you to physically tour the property while adhering to social distancing rules? What if the desired property is occupied and the current tenants do not want the added exposure of strangers? Some may have the ability to wait out this near-term uncertainty and move into a new home or apartment later down the road. Others, who must move within the next year or so may see themselves forced into a practice seen only in our country’s major metropolitan areas or if relocating hundreds or thousands of miles away – renting sight unseen. As technology has advanced to make virtual touring of rental apartments and homes a possibility, it has also allowed for an increase in the possibility for rental fraud. If you are a prospective tenant traversing this new virtual landscape, beware of deals too good to be true or go against your gut instinct. Let us look at some of the common scams out there and then see what steps you can undertake to protect yourself against fraudulent activity. Rental Fraud is Real! Let me begin by assuring you that rental fraud is real. This is not some “Boogey Man” created by an anti-tech movement bucking against the evolution of the industry. Even before the COVID-19 pandemic and social distancing measures, rental fraud had cost U.S. renters millions of dollars. A 2018 Rental Fraud survey from Apartment List found that fraudulent activity impacts millions of renters. An estimated 5.2 million U.S. renters were defrauded, and the national survey of renters found that well over 40% of renters reported either discovering or encountering fraudulent listings while searching for a new apartment. This is just a snapshot of the growing threat rent fraud has become all over the U.S.. Now COVID-19 has created a new environment that gives another advantage to scammers as in-person tours and interactions with landlords and property managers will be more difficult. This extra layer will make it even harder for renters to determine which listings are legit. However, there are some definite red flags you may come across during your search. Here is what to look for and how you get around them. The Most Common Red Flags! 1. Too Good to be True If you see a listing with “out-of-this-world” amenities asking for considerably below-market rent in a hot real estate area, be skeptical rather than think you just hit the lottery. First, use Google or Apple Maps – or some other map platform - to make sure this is an actual property. Second, see if there is another listing for the same property with a higher rent. We have seen in our own property management dealings where scammers will copy listing details and create their own lower priced post. 2. Upfront Requests for Payment or Financial Information that Seem Odd Beware of anyone pressuring you to send money immediately to reserve a property because of all the interest they have received. Also, be wary of a reluctance to provide customary information or virtual tours without receiving payment first. A typical part of the renting process are background checks. It is necessary for landlords and property owners to validate you are who you say you are. However, there is no past so sordid that the cost of a background check would be upwards of the $45 - $60 range. If so, be very cautious going forward. 3. There is a Reluctance or Inability to Provide a Lease If a supposed landlord or property manager objects or has excuses as to why he or she does not want to enter into a written rental agreement, there should be red flags. Even short-term or month-to-month leases will require written documentation. How to Protect Yourself Against Rental Fraud 1. Research! Research! Research! Even as technology has made it easier for rental fraud, it has also given renters the ability to do their due diligence in finding legitimate apartments and housing. Research comes in the form of looking up and verifying property managers through reviews on multiple platforms and sending out a “Bat Signal” to all your colleagues and friends on social media pages. These resources should be used as points of reference during the decision-making process. 2. Ask for a Virtual or 3D Tour and/or a Multitude of Photos Once again, make technology your friend. As previously stated, even prior to the COVID-19, virtual and 3D touring of properties was trending. Now this option becomes a necessity as stay-at-home orders have been imposed across the U.S. and current tenants have a reluctance about letting strangers in their home. Virtual tours can be used to verify that the property owner or manager is who they say they are while also revealing certain nuances of the property. If the landlord or property manager can not provide a virtual tour, request as many detailed photos as possible. 3. Steer your Searches to Reputable Property Management During a time of unknowns, do you really want to put your future living situation in the hands of another unknown variable? Reputable, known property management will make the sight unseen renting experience a little more palatable as they should be easier to research, contact and provide you with all the needed resources discussed earlier.

About six years ago I had the opportunity to write about some of Baltimore’s social, political and economic issues for a local alternative website. This was pre the Freddie Gray unrest and Catherine Pugh scandal. Even before the last five years of turmoil, Baltimore – like similar urban areas – had its issues. At one point, my focus revolved around the lost sense of community that permeated many Baltimore neighborhoods. How could we bring back that pride that motivated homeowners to scrub down stoops and sweep their gutters every weekend? I remembered this civic pride when I was growing up and thought a return to that type of spirit could bring about a broader change in many challenged communities. I scoured through several websites and newsletters looking to see what other municipalities and cities had implemented to solve such problems. And then I found something. Make renters stakeholders In Cincinnati, OH, a non-profit community development organization got innovative with the relationship between property managers and tenants. The Cornerstone Corporation for Shared Equity (CCSE) created a program where the tenants of CCSE owned and developed properties entered into a contract in order to earn “equity credit”. To understand equity credit, think of your 401(k) plan’s vesting schedule. As you contribute to your plan, there is an ownership schedule to what’s contributed. Usually you can be 100 percent vested – defined as full ownership to all the assets in your account - within a certain amount of years disclosed by the 401(k)plan agreement. Think of rent payments as retirement contributions - accumulating over the length of a tenants stay at a property. Ultimately, the tenant gains ownership over those accumulated payments if the requirements of the lease are fulfilled. Equity Credit gave tenants “skin in the game”. As new stakeholders in the community, the State of Ohio found that the system kept rent prices down along with bringing about an average 96 percent occupancy rate over the first 12 years of the program. This was good for both tenants and property managers. If you would like to learn more details on the program, my original article can be found at the following link https://baltimorepostexaminer.com/change-baltimores-neighborhoods-make-renters-stakeholders/2014/10/16 So why revisit an article from 6 years ago? The Affordable Housing Crisis The idea of equity credit, or re-imagining the property manager/tenant dynamic, may make even more sense as America faces one of its new crises - affordable housing. Over the past few years, non-profits and academic institutions have made the case for the severity of this crisis. The Urban Institute found that for every 100 extremely low-income households in need of an affordable apartment, there are only 29 available units. The Harvard Joint Center for Housing Studies presented research that nearly 39 million households are cost-burdened- in effect paying nearly a third of their income for housing. Reports by the National Multifamily Housing Council (NMHC) and National Apartment Association (NAA) forecast that the U.S. will require 4.6 million new affordable housing units by the end of this decade. In 2013, the founder and property manager of CCSE, Margery Spinney and Carol Smith respectively, founded Renting Partnerships to utilize what they developed at Cornerstone on a broader scale. In a 2018 interview with YES! Solutions Journalism, Spinney stated, “There’s never going to be enough government funding to provide affordable housing for everybody… We are not replacing home ownership and we’re not going to replace renting. We’re really creating a third kind of housing.” In cities like Baltimore, innovative processes can use property management as a vehicle of change in communities that periodically are ignored. The dialogue always centers around finite space, development costs, zoning and municipal legislation. What may save metropolitan areas across this country is creative problem solving in both social impact development initiatives and property management using our current inventories. As developers create high-end multi-family units with the lure of amenities, may be affordable housing can flourish out of the desire for community. Rather than enter the market by means of government subsidies or other programs, a local grass roots effort could nurture organically throughout pockets of the city. We know the market is there. And for the property management world, diversification – if not currently a part of your portfolio – into the affordable housing market makes social and economic sense. It can be a WIN/WIN solution for all of us.

Your property is not your home; it is a business venture If you purchased a property for the specific use of rental income, this is probably not news to you. If you decided to rent out your home, you must come to the realization that it is no longer the first home you bought or the place you raised a family. It is now an investment business and its primary role is as a source of income. As with all businesses, you must be professional and compliant The fundamentals of becoming a landlord are composed of two parts: the property and the tenant. This premise seems easy enough, but the devil is in the details. Let’s start with the product you deliver: your property. In many municipalities you just can’t wake up one day and rent your or any other house. In both Baltimore City and County, all residential units must be registered, inspected and licensed to ensure they meet safety and maintenance standards. Typically, inspectors will look for “basic life, health and safety items to insure the property is up to code and safe for the occupants and neighboring residents, including but not limited to electrical, plumbing, smoke and carbon monoxide detectors, interior and exterior sanitary conditions, utilities, and lead paint” – to borrow Baltimore City’s Department of Housing & Community Development language. Once your property is up to code, then it’s necessary to have a plan in place of how you will tackle any issues going forward. What happens if the furnace or hot water heater goes down in the middle winter? Who should be called if a pipe bursts and floods a basement? What procedures should the tenant need to follow if they lock themselves out late at night. As we stated before, this is a business. Protect your income stream. Find the right tenants. Before we get into credit scores and background checks, there is one thing a landlord needs to do to ensure the right tenants. They need to set the right price for rent. The landlord needs to do their due diligence in finding comparables in the area that reflect the rent range you should be able to charge. This should be a market driven and/or financial decision. Allowing emotion or other factors to creep in can keep your property vacant. Vacant properties are not good for business as they cost money without bringing any in. The combination of a standout property correctly priced should bring the preferred tenants you are looking to find. However, every prospective tenant is not who they appear to be. You now need to put in place the proper vetting system. The following are all variables that should be used in the tenant decision-making process: • Consistent income • Rent to Gross Income • Rental History • Credit Check • Background Check (Finding good tenants is a topic all its own and will be tackled in future posts.) Being a Landlord might seem a bit overwhelming If all this – which includes preparing your property for market, making sure your property is in compliance with all applicable laws, marketing your property, collecting rent payments and dealing with tenant issues and complaints – seems a little daunting, you may want to hire a property manager. Managing property is time consuming and professionals could alleviate some stress while making your management processes more efficient. A good property manager could also make it easier for you to grow your portfolio. As with all aspects of property management, finding the right property manager requires due diligence to find the right dynamic between owner and manager. If you have thought about becoming a landlord or find yourself overwhelmed managing a property or portfolio, feel free to reach out to Canton Management Company at (410) 342-2205 or visit our website at https://www.cantonmanagement.com/ Happy Managing,

The Baltimore rental market: 2010 - Present As we usher in a new decade, let’s look back at the ten years that just passed. Baltimore City experienced a roller coaster ride socially, economically and politically. So much happened that we don’t have the time or space to discuss it here. However, for real estate agents, property owners, managers and investors, the residential rental environment took a dynamic turn. Over the past five years, friends, family and Uber and Lyft drivers have all asked, “What’s up with building all these apartments downtown?” And it’s just not downtown proper, it’s a phenomenon happening in all the waterfront neighborhoods. After decades of wandering in the woods, did City development finally find its way through the trees? With strong demand during the beginning of the last decade, 2014 saw Baltimore City approve legislation that gave developers a fifteen-year tax credit to convert underutilized space into residential units. A key aspect of the law allowed developers to get a pass on paying taxes on the first two years of their project. The re-imagining of century old architecture was not the only space where this boom would occur. The last five years saw the planning and development of luxurious projects built from the ground up in the waterfront communities encircling downtown. From 2012 – 2017, the Downtown Partnership of Baltimore released data showing that nearly 5,200 new apartments and condos came on the market. For the entire decade, the Baltimore Business Journal reported about 14,000 new Class A luxury multi-family units were added to the City. You hear talk that developers will only build luxury housing these days because that’s the only way to get a necessary return on investment. This is part of the equation. The other part is demand. For this much development, you need a lot of demand. Who’s living in these places? There has been a steady increase in income growth among downtown residents. According to Yardi Matrix’s “Steady Baltimore: Multifamily Report Summer 2019”, the Baltimore metropolitan area gained 11,700 jobs from June 2018 – June 2019. In fact, the Professional and Business Services, Education Health Services and Manufacturing sectors created 17,400 jobs alone – offsetting losses in other industries. The expected future growth in areas like Technology gives no reason to stop building downtown and in the surrounding areas. Professionals working downtown, Millennials and empty nesters value “walkability” and are attracted to the amenities being offered by these newly constructed or remodeled units which include: 24-hour concierge, community kitchens and bars, business lounges, state-of-the-art-gyms, yoga studios, salons, theaters, pet park and runs, pools and community and resident gardens. Units lease from $1200 a month for a one bedroom to over $8000 per month for penthouses. Gone are the days when investors could buy a rehab rowhome in the Canton and Federal Hill neighborhoods and demand any desired rent. There is still a priority to live in these neighborhoods, however luxury apartments are creating a sense of “inner” community within their communities. And more luxury units are coming. Some of the latest data show there are over 2,200 new apartment units under construction as of September 2019. And it’s not just happening here? The trend is being played out across multiple metropolitan areas throughout the country. Apartment List's Rentanomics put out a paper last year were they tracked high-income renter households. This group, whose annual income floor was $100,000, was the fastest growing segment of the housing market – with a national growth rate of 48 percent from 2008 – 2017. Some mid-sized metropolitan areas like Denver and Austin have seen this number grow as drastically as 146 and 142 percent respectively. Since the Financial Crisis, Baltimore itself has seen this demographic of renter households rise by 40 percent. On the high-end, supply is holding rents at bay. But supply at the other end of the rental market could start driving prices up due to high occupancy rates. In conjunction with occupancy rates, data shows nationally that since 2008, renters are staying in the mid to low rent property range longer compared to before the Crisis. Some solutions need to be figured out This cannot go on forever. Urban areas are finite spaces. At some point, due to income inequalities and a lack of affordable housing, some local or federal policy may have to be involved. Or we can hope some urban planning genius comes up with an idea that leads us into a new way of city living for the rest of this Century. If you’re looking to rent in Baltimore or another urban area, I hope this gives you a clearer picture of the environment. Property managers and investors in cities – with an established portfolio or just starting out – may want to have a conversation with someone and figure out a plan going forward.